Salve, cari subscripti!

Thank you for reading this week's edition of Closelook@Hypergrowth, dated November 14, 2024 👋. The next edition will be published on 20 November 2024.

A Closelook At This Edition

This Week's Action: Trump Winners and Losers

Macro Insights: Sticky Inflation Landing Ahead

Higher For Longer: Initial Macro Forecast For 2025

The Hypergrowth Portfolio: Rebalancing After Earnings And Election

This Week's Stock Spotlight: Zeta Global - Fraudulent Financials?

Knowledge Corner: Why 2024/25 is different from 2016/17

Upcoming Transactions: More Rebalancing After the Election

Final Words: It’s The Bond Market, Stupid!

(1) This Week's Action: Trump Winners and Losers

Stocks have been on a tear since Donald Trump claimed victory in the United States election last week. The S&P 500 posted its best week in a year, gaining 4.7 percent and crossing the symbolic threshold of 6,000 for the first time.

The Nasdaq and the Nasdaq 100 finally made new ATHs, breaking above the summer 2024 highs.

The best-performing Nasdaq 100 stock in the past month has been Tesla - up more than 50 percent. Animal spirits have returned.

The table below shows the Nasdaq 100 one-month individual stocks performance ranking.

Quite a few semiconductor stocks are at the bottom of the table, while software has finally outperformed the hardware/infrastructure-related AI sectors.

Super Micro, Moderna, and PDD have been the worst performers - all for different reasons.

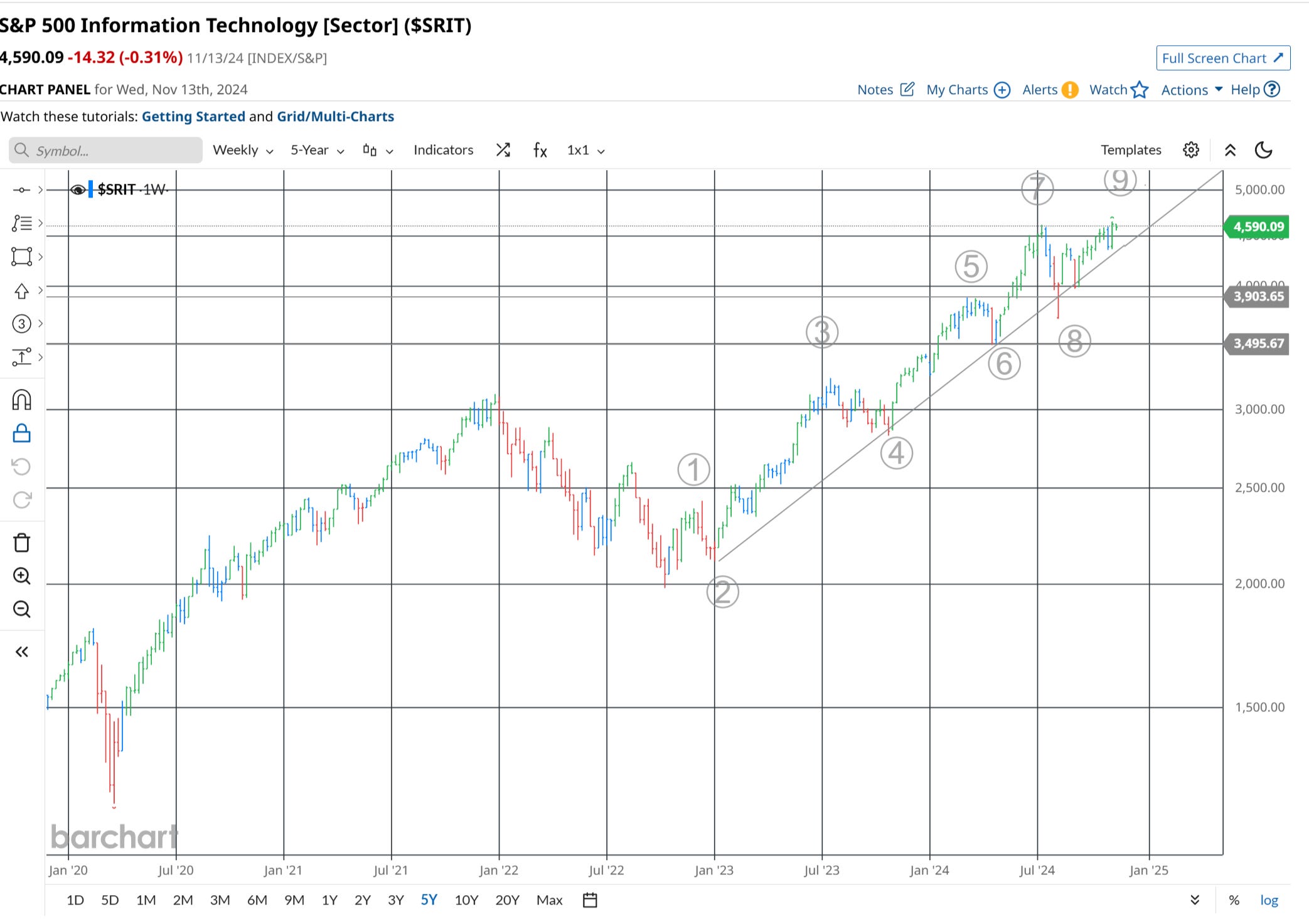

In contrast to the two NASDAQ indices, the performance of the SP 500 Info Tech sector has been more muted (which is a warning signal to me).

I see the sector in the midst of completing wave 9. This may indicate a forthcoming top as the minimum requirements for a 5-leg impulse wave setting with extension have been satisfied.

While we are entering the seasonally best 10 weeks of the year (mid-November until the end of January), I am worried about the bond market's performance.

The 30-year fixed mortgage rate yields have risen to 7.38 % from around 6 percent at the time of the initial Fed cut.

The TTL ETF has cratered. It is trading below 90 USD and heading toward the central support zone around 87.50 USD.

It may well have completed an A-B-C consolidation pattern, followed by (the early stages of) another impulse leg down. In a more bullish scenario, yields should stop rising around the current level and move back to the 100 USD level (see A-B-C-D-E pattern above).

In a bearish scenario, yields will soon cross the 4.50 percent level and move closer to the 4.75 to 5.00 percent level.

(2) Macro Insights: Sticky Inflation Landing Ahead

Trump vs. Bond - the real battle will not be between the Democratic Party Leaders and Big D; the newly elected president will face a more challenging opponent.

The name is Bond - Treasury Bond! The real battle will be between the bond vigilantes and Donald Trump. And bond vigilantes are tough adversaries. They cannot be scared away by social media, (false) claims, or any other measures from the political campaign playbook. They like to make a deal, lock in a profit and disappear.

Yesterday's CPI report indicated inflation might become sticky above the Fed's 2.0% target. Headline and core CPI inflation rates increased to 2.6% and 3.3% year-over-year in October.

While goods prices continue to deflate, supercore inflation, rent inflation, and wage growth all saw increases last month, suggesting they are stabilizing at relatively high levels.

This, combined with strong economic growth, lends further evidence that the Fed may not ease monetary policy a lot further in the months ahead. This view is further reinforced by rising bond yields, which question the wisdom of the Fed's recent rate cuts.

One and done! One rate cut in 2025 and no more is my preferred scenario.

Ed Yardeni is not concerned about a second wave of inflation, as he believes that increasing productivity is already enhancing real GDP while containing unit labor costs inflation.

Recent upward revisions in productivity support this perspective. However, Yardeni suggests that the Fed may need to allow more time for consumer price inflation to become less sticky before considering additional rate cuts.

Ed Yardeni lifted his SP 500 targets to 6,100 for this year, 7,000 for 2025, and 8,000 for 2026. While I still align with this bullish view, I have raised the probability that we will see a much worse stock market performance in 2025.

One reason is that the bull market will be entering its third year in 2025 - this often marks the end of a bull cycle. The second reason is that while earnings have risen and are projected to continue increasing in 2025, valuations in anticipation of lower interest rates have risen even more.

Multiple expansion has contributed to more than fifty percent of the SP 500 advance in 2024.

This has been based on projecting much lower rates in 2025, as the Fed Dot Plot outlined numerous rate cuts ahead.

Assuming this will not happen, we may see multiple compression in 2025 offsetting any positive effects from rising earnings.

I think it will all depend on the bond market, where we may see the “higher for longer” views re-emerge as soon as December 2024.

(3) Higher For Longer: Initial Macro Forecast For 2025

In the U.S., several factors contribute to the concern about a potential uptick in inflation in 2025, particularly when compared to 2024 numbers.

Sticky Inflation

Inflation, especially in the service sector, is showing signs of becoming sticky. This means that despite overall inflation rates slowing down, specific components of inflation are not decreasing as quickly as expected. Services inflation, in particular, is stubborn and continues to be a concern.

Supercore Inflation

The supercore inflation measure, which isolates components of core inflation that are highly sensitive to economic conditions, has been rising. This indicates that demand-driven inflationary pressures are persistent.

High Rents and Housing Costs

Shelter inflation, which includes rents and owners' equivalent rents, remains elevated. Although there was a slight deceleration in shelter costs in some months, they have not cooled as quickly as anticipated. Housing insurance costs are also increasing due to more frequent and expensive natural disasters, contributing to the stickiness in housing-related inflation.

Structural Changes in the Economy

Structural changes, such as labor shortages, especially in industries requiring in-person work, and the aging of the U.S. population, are driving up costs for health care services, health insurance, and other services. These factors resist the Federal Reserve's efforts to drive inflation back to the 2% target quickly.

Comparison to 2024 Numbers

The year-over-year comparison of inflation rates in 2025 will be influenced by the inflation rates experienced in 2024. The base effect could make the year-over-year inflation rates in 2025 appear higher.

Federal Reserve's Stance

The Federal Reserve may turn more cautious about cutting interest rates due to the persistent inflation, particularly in the service sector. While there are forecasts for potential rate cuts in late 2024 and 2025, the Fed may wait for further cooling in inflation before making any significant moves.

The path to achieving the Fed's 2% inflation target may be slower and more challenging than anticipated, leading to concerns about an uptick in inflation in 2025.

The reflationary policies anticipated under a second Trump administration could significantly impact the economic landscape, particularly in the context of adding to inflation concerns.

Inflationary Pressures

Trump's policies, including tax cuts, increased infrastructure spending, and protectionist measures such as tariffs, are expected to drive inflation. Tariffs, in particular, can lead to higher consumer prices as the costs of imported goods increase.

Reducing the labor pool due to stricter immigration policies could also contribute to inflation by reducing the supply of workers, potentially leading to higher wages and prices.

Fiscal Policy and Debt

The Trump administration's plans for tax cuts, such as extending the Tax Cuts and Jobs Act of 2017, will likely increase economic growth and lead to higher fiscal deficits and national debt. This could exacerbate inflationary pressures and create uncertainty in the markets.

Monetary Policy

The Federal Reserve may need to adjust its monetary policy in response to these reflationary measures. Higher inflation expectations could lead to higher interest rates to control inflation, which would impact bond markets and the overall cost of borrowing.

Market Reactions

The anticipation of these policies has already led to market reactions, such as higher yields on 10-year Treasury notes and a stronger US dollar in the short term. However, long-term uncertainty around trade policy, fiscal deficits, and inflation could further challenge bond markets.

Labor Market and Immigration

The impact of stricter immigration policies on the labor market could be significant. While some analysts argue that the reduction in the labor pool might not immediately lead to wage pressures due to existing slack in the unskilled labor market, others warn that mass deportations could disrupt the social and business fabric and lead to higher costs and inflation.

Reflationary Trades

Reflationary policies of the Trump administration are expected to:

Increase inflation due to tax cuts, tariffs, and labor market adjustments.

Lead to higher fiscal deficits and national debt.

Influence monetary policy, potentially resulting in higher interest rates.

Impact various market sectors differently, with equities likely benefiting and bond markets facing challenges.

Create uncertainty and volatility in financial markets due to trade policy and immigration changes.

Investors are already positioning themselves for a reflationary environment, with markets pricing in higher inflation and interest rates.