NVIDIA 2030: The Operating System of Global Intelligence

Why the consensus is mispricing the most important infrastructure build in economic history

The Thesis

NVIDIA is not riding a cycle. It is becoming a utility — the first technology company on a credible path to one trillion dollars in annual revenue. Not because demand stays hot, but because NVIDIA is transitioning from selling hardware to operating the base layer of global compute. Every inference call, every agent transaction, every digital twin simulation, every robot brain update runs on NVIDIA's stack. That is not a product cycle. That is a tax on intelligence itself.

The market prices NVIDIA like a semiconductor company with unusually high margins. The correct framing is a technology utility with structural lock-in, recurring software revenue, and sovereign-grade demand. The gap between those two valuations is where the alpha lives.

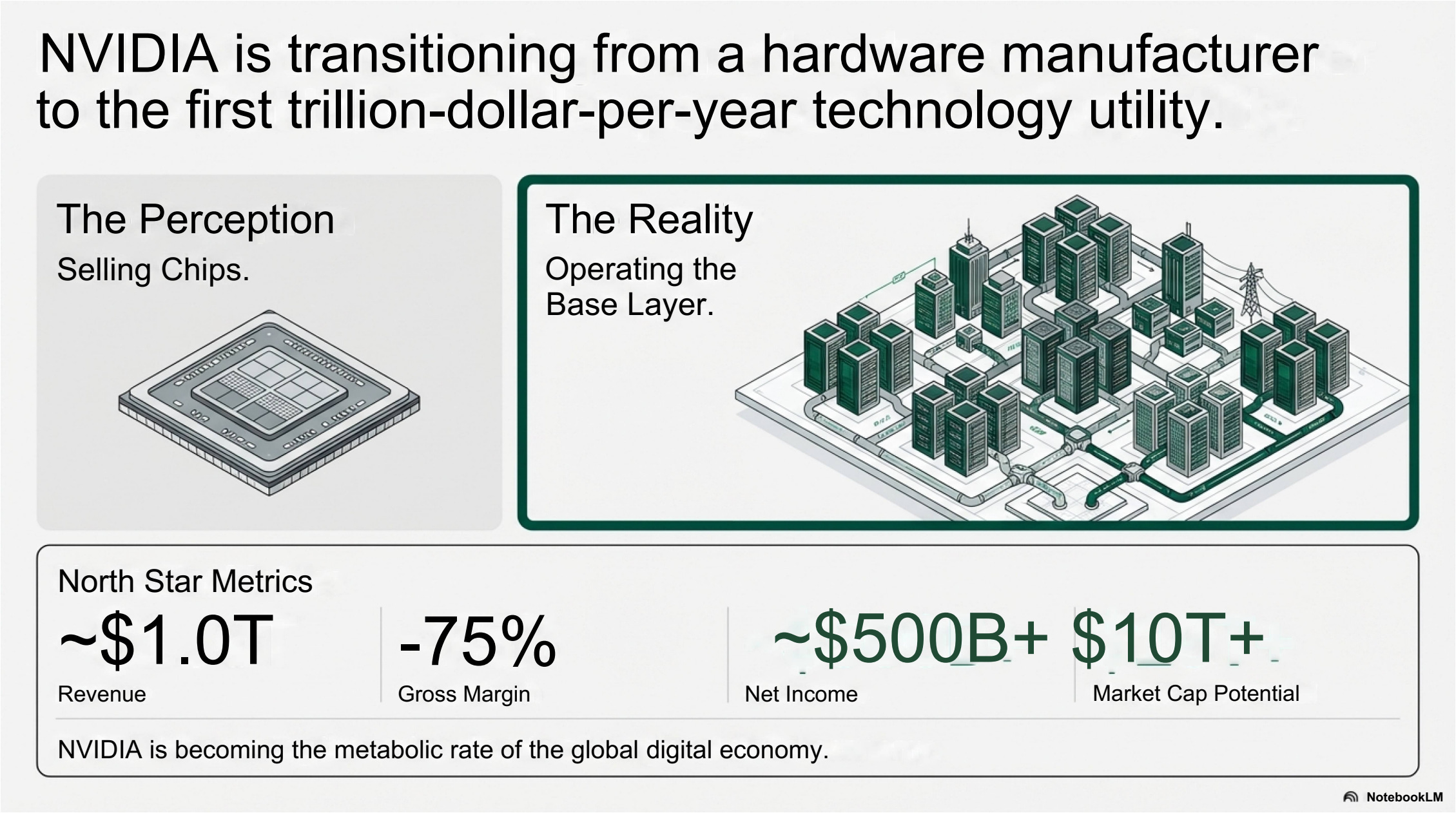

What The Market Sees vs. What's Actually Happening

The Perception: NVIDIA sells GPUs into a hot market for AI training. Demand is cyclical. When hyperscaler CapEx normalizes, margins compress, and revenue declines. This is a chip cycle, and chip cycles end.

The Reality: NVIDIA is building the infrastructure layer that every AI workload — training, inference, agentic, physical — must run through. The CUDA ecosystem, NVLink fabric, and software stack (NIMs, Omniverse, AI OS) create a lock-in that deepens with every generation. Customers don't buy chips anymore. They buy sovereign AI factories.

Revenue 2025E: ~$130B → Revenue 2030E: $900B–$1T

Gross Margin: ~74% → ~75% (stable)

Software ARR: ~$5B → $120–140B (28x growth)

Net Margin: ~45% → ~55% (expansion through software mix)

The margin story is the key that most analysts miss. Software ARR scaling from $5B to $140B acts as a high-margin buffer against any hardware commoditization. NVIDIA's blended margin improves as it sells more software, not less hardware.

The Historical Pattern

Every major computing era produced one dominant platform layer.

Microsoft established a monopoly in the operating system market for personal computing. Apple built the consumer platform that owns the interface between humans and devices. AWS created the global cloud utility that commoditized infrastructure. NVIDIA is building the next layer: the global intelligence utility that powers training, inference, agents, and physical AI across every industry and sovereign boundary.

The pattern is consistent. Each layer captured a disproportionate share of the value created in its era because it was the chokepoint — the one piece of infrastructure that everything else depended on. Windows took a cut of every PC sold. iOS took a cut of every app purchased. AWS takes a cut of every workload hosted. NVIDIA is positioning to take a cut of every computation that involves intelligence.

By 2030, NVIDIA will operate the base layer of compute, the OS for autonomous agents, the network fabric for planetary-scale inference, and the sovereign infrastructure stack for nation-states. That is not a chip company. That is the operating system of civilization.

The Structural Moat

Three interlocking mechanisms make NVIDIA's position far more durable than a typical hardware lead.

Forced Upgrade Cycles

NVIDIA has compressed its architecture cadence to roughly 12 months: Blackwell (current) to Rubin (2026) to Feynman (2028). Each generation delivers performance improvements so large that the previous generation becomes economically unviable within 24 months. This is not Moore's Law — it is Moore's Law on steroids.

The secondary market for AI accelerators collapses because no rational buyer purchases hardware that will be 3–4x less efficient within a year. The result is permanent demand scarcity and continuous pricing power. Every customer must upgrade. There is no "good enough."

The Software Tax

NVIDIA's software stack — CUDA, NIMs, Omniverse, and the emerging AI OS layer — creates a 90% margin annuity that sits atop the hardware base. Every inference call is a taxable event. Every agent transaction is a taxable event. Every digital twin simulation is a taxable event.

Software ARR is projected to grow from approximately $5B today to $120–140B by 2030. That is a 28x expansion in recurring, high-margin revenue that transforms the financial profile from hardware cyclical to utility compounder.

Complexity as Margin Shield

NVIDIA no longer sells chips at transparent per-unit pricing. It sells racks at $4M, clusters at $1B, and sovereign cloud deployments at $10B. Each package bundles compute, networking (Spectrum-X, NVLink), cooling infrastructure, security, and software into a single deal. The complexity of these packages makes margin extraction invisible to buyers and analysts alike.

You cannot reverse-engineer the GPU margin from a billion-dollar sovereign AI factory contract. That opacity is structural and intentional.

"NVIDIA no longer sells chips. It sells national AI factories."

The sovereign angle adds a dimension that pure enterprise demand cannot. As trust in US hyperscalers erodes geopolitically, governments become the new whale customers. National AI clouds, defense-grade infrastructure, autonomous city platforms, and data sovereignty requirements all funnel through NVIDIA as the neutral geopolitical utility. This is infrastructure spending that is politically durable and not subject to corporate CapEx cycles.

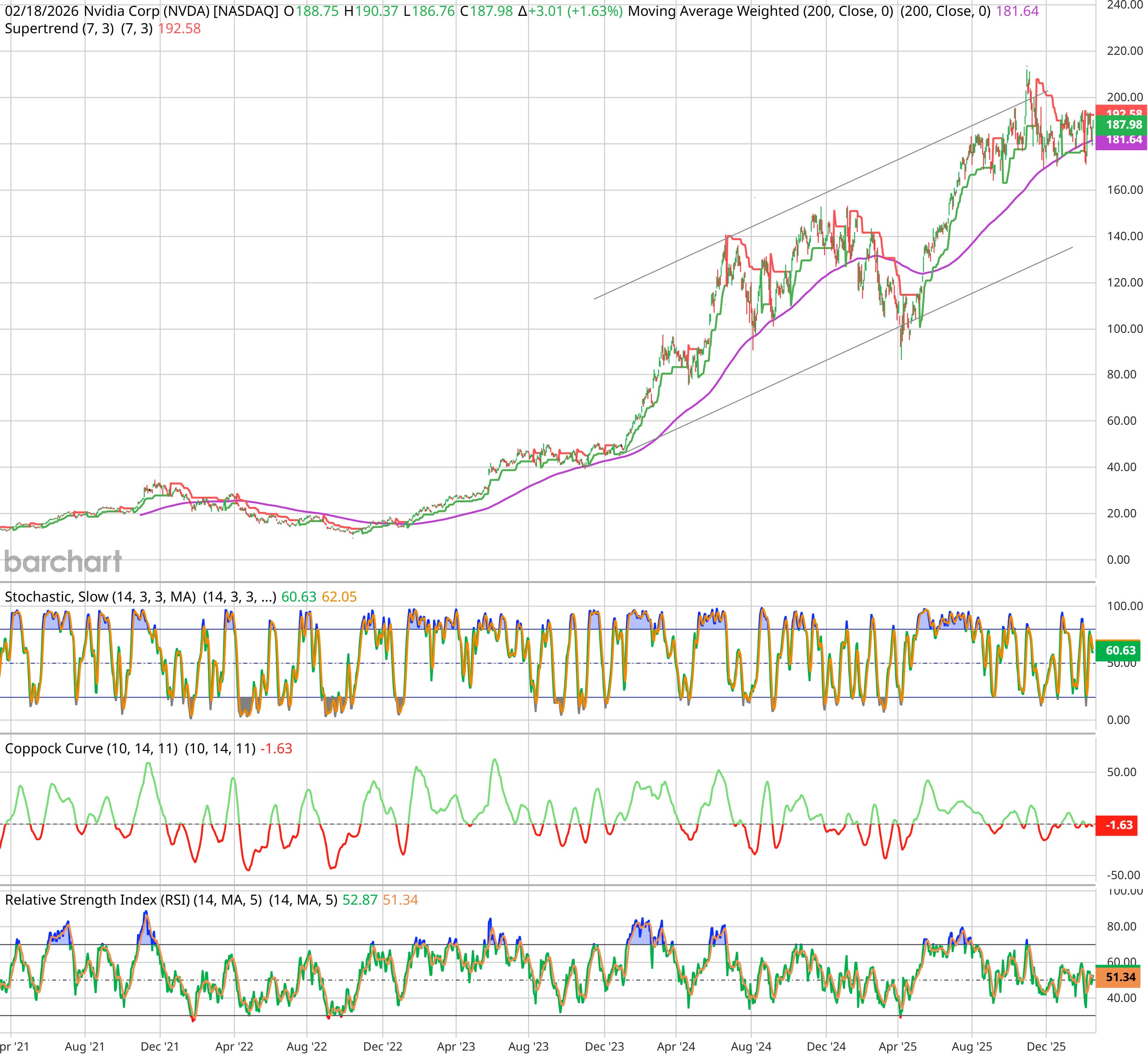

Technical Setup

Trend: 🟢 Bullish

Structure: Trading above rising 20W and 50W EMAs. Held breakout above prior all-time high after January consolidation. Higher lows intact since October 2023.

Key Levels: Support $180 / $160 — Resistance $195 / $215 zone

Volume: Confirming on breakout candles, declining on pullbacks — healthy accumulation pattern.

Signal: The weekly structure supports the fundamental repricing thesis. The market is gradually shifting NVIDIA from semiconductor multiples toward platform/utility multiples, and the chart reflects that in the persistent bid under every consolidation.

What's Below The Surface

The thesis and the moat are clear. But the real questions for investors are: what exactly does $1T in revenue look like, segment by segment; what breaks the thesis; and how do you size the position?

In the C+ Premium section on Substack, we go deeper:

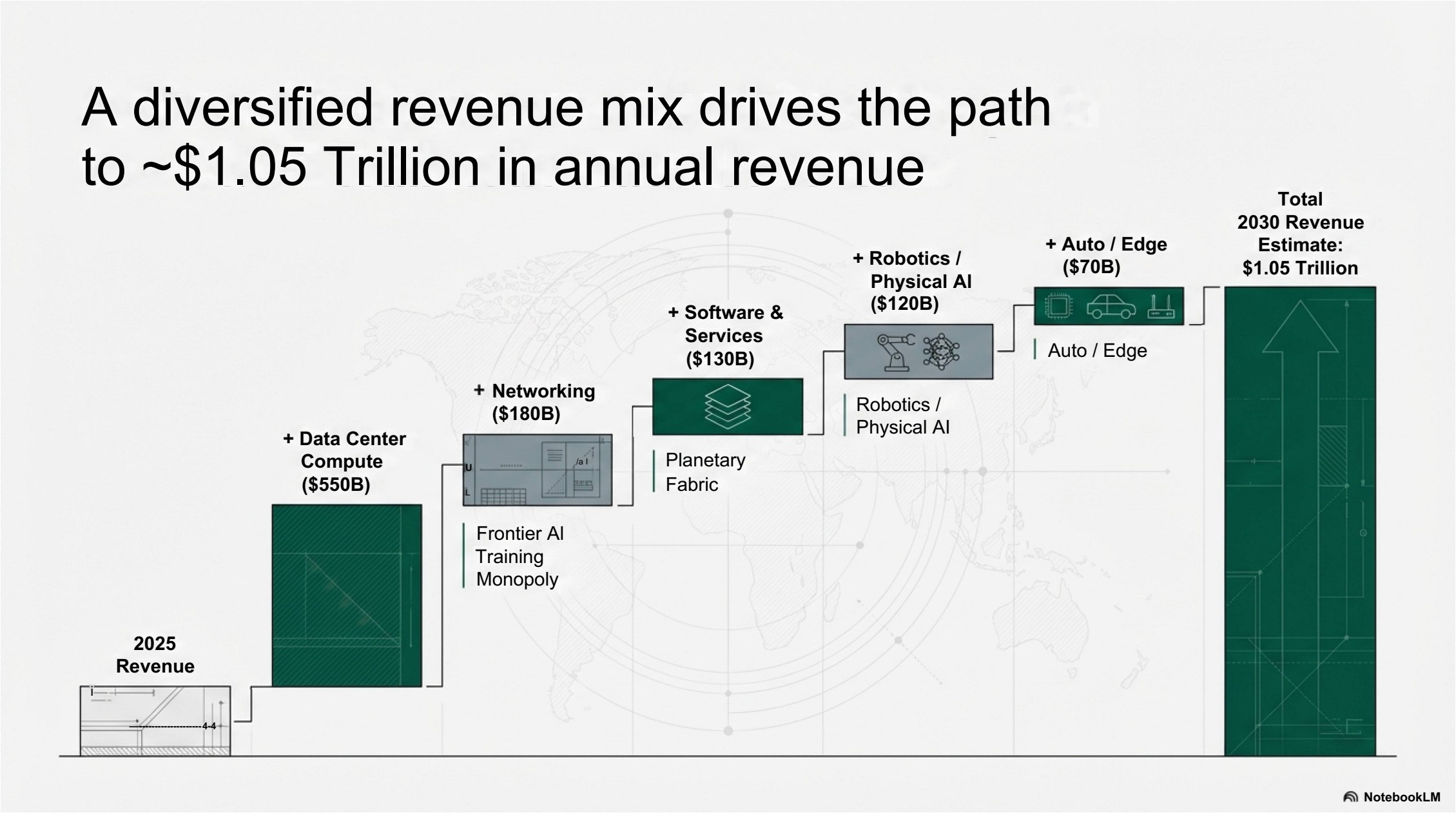

→ Full revenue waterfall: $550B data center + $180B networking + $130B software + $120B robotics + $70B auto/edge

→ Bear ($5.7T) / Base ($13.1T) / Bull ($15.8T) valuation with implied share prices

→ Three macro waves: Data Center Replacement, the Agentic Economy, and the Robotics Economy

→ The Canary Risk Framework: Custom ASICs, Rubin yield issues, sovereign regulation, Taiwan geopolitics, and power grid constraints

→ Portfolio: NVIDIA is a core position in the Closelook Hypergrowth Portfolio. Live tracking coming soon for C+ Exclusive subscribers.