Stretched Semis, Soft Macro, Narrow Breadth — Trim, Roll,

Weekly Portfolio Updates

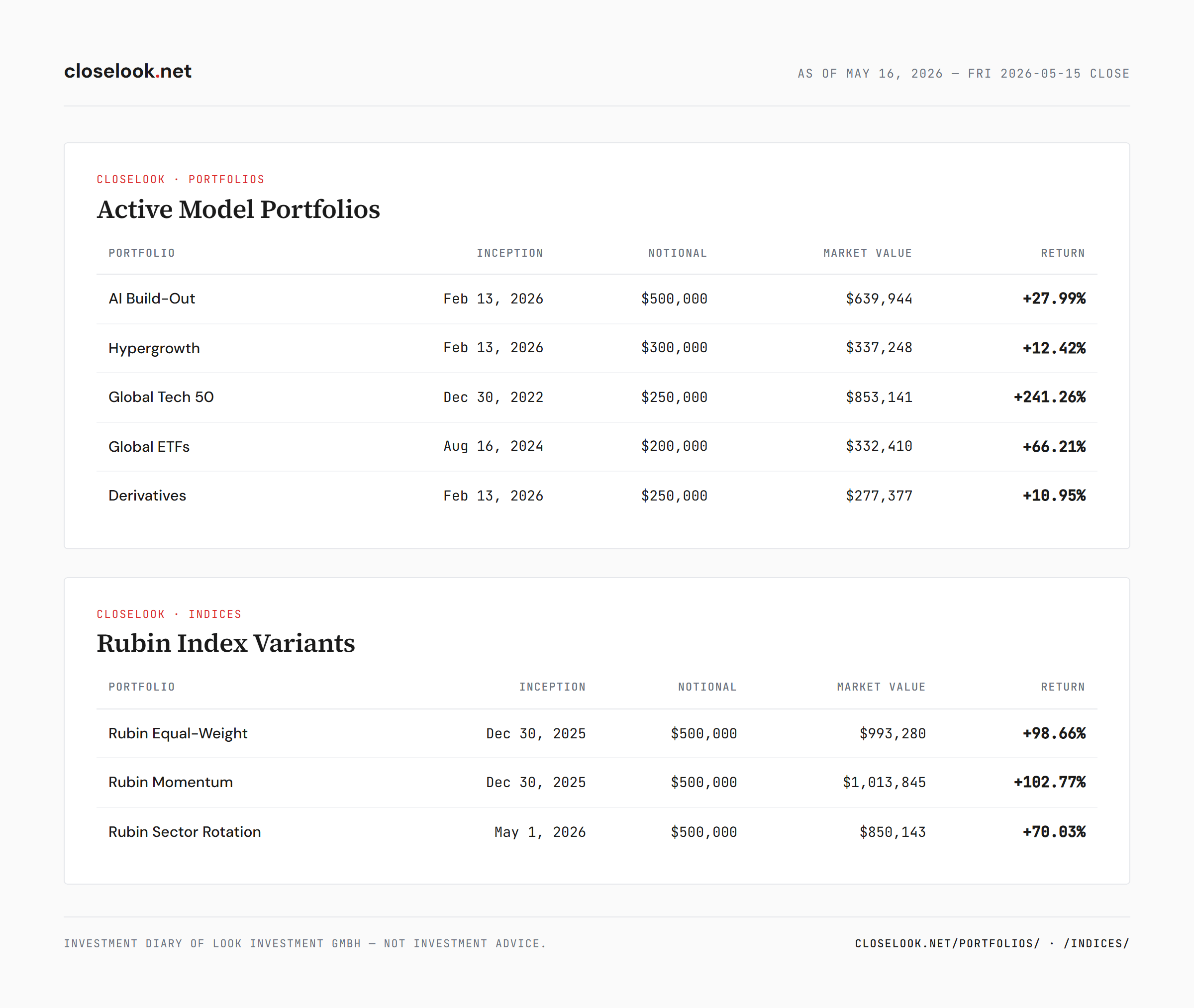

Saturday, May 16, 2026 · Closelook Signals

This week was about defense-in-position. After last week’s broad trim, the book moved into a deliberate posture: roll up and out where conviction is intact, take fresh long-side exposure only where the chart finally gave us an entry, keep harvesting premium on names we want to own cheaper. Five portfolios, ten transactions, none of them random.

https://closelook.net/portfolios/

The Hypergrowth book carried the heaviest activity. Six option positions got rolled up and out on Wednesday, all in the same direction — closer-to-the-money near-dated calls covered, deeper out-of-the-money longer-dated calls written. AIQ from August 2026 50-strike covered up to January 2027 65-strike. ASX from September 2026 30-strike up to January 2027 40-strike. DDOG from January 2027 175-strike out to January 2028 210-strike. RKLB from December 2026 110-strike out to March 2027 150-strike — and the size came down from two contracts to one, which is the closest thing to a partial-trim on this side of the book. SMHX from July 2026 45-strike out to October 2026 60-strike. NU January 2027 17-strike just got closed cleanly — the gain on a sub-dollar call wasn’t worth carrying into the next cycle.

What does six rolls in one day look like? Bullish-but-disciplined. Every roll moved the strike higher AND the expiry later. The premiums received on the new contracts more than cover the cost of closing the old ones in most cases, so this is roughly cash-neutral while keeping the same direction of exposure. The two RKLB strikes, in particular, walked from 110 to 150 — that’s a 36% lift on the same name. Either RKLB keeps running and the new calls follow it, or they expire worthless and we keep the premium. The asymmetry sets up the way we want it.

The single new long this week sits in two books: GLW (Corning Inc.), 100 shares each in AI Build-Out and Hypergrowth at $190.94. Corning is the optical-fiber and photonics name that earns when AI training and inference scales. Every Rubin rack ships more glass, more co-packaged optics, more interconnect substrate. The thesis isn’t new — what changed is the chart finally let us in without paying through the nose. We added it to two books because Corning fits both narratives: structural beneficiary of the AI build-out, and a momentum name that has cleared resistance with breadth confirmation in the interconnects complex this week (the Rubin Interconnect sub-index closed the week +13.26%, even after Friday’s red day took some heat off).

Global ETFs got the only meaningful rotation. Out of REMX — the rare-earth/strategic-metals basket — locking in a $1,081 gain. Into IYM (broad US basic materials), ICOP (copper miners), SGRT, and TINY. The reasoning here is sector-rotation, not stock-picking. Rare earths were the right exposure when the China-trade-war narrative was peaking; copper, steel, and broader materials are the right exposure if global capex re-accelerates and inflation prints stay sticky. The materials complex has been the quiet relative-strength story underneath the semi headlines — and it isn’t a one-week move. Copper is breaking out, base metals are tracking with industrial production. The rotation makes the ETF book more cyclical without changing its size.

Derivatives ran one closeout and one open. Closed two RKLB January 2027 80-strike puts for $11.20 each, locking in a $3,328 gain. Those puts were sold short during the RKLB drawdown earlier this year; the name has now recovered enough that holding the premium to expiry was no longer the right use of capital. Sold one NET January 2027 175-strike put short for $26.30, banking $2,629 in premium. NET sold off hard on Friday May 9 after their print — we’d be happy to own it at an effective net cost south of $150 if it gets there. That’s the volatility-harvesting engine doing exactly what it’s designed for: extract premium on names we want to own cheaper, with strikes set at prices that make the entry attractive whether the put gets assigned or expires worthless.

Global Tech 50 had one mechanical transaction: SAP dividend reinvest, 0.65 shares at $169.48. Nothing discretionary. The portfolio compounds because every dividend is reinvested at the prevailing price — across 48 names over five years, that’s where a large fraction of the total return comes from.

Now the macro.

The setup heading into next week is uncomfortable. Semis ran hard through Wednesday and Thursday, then Friday took a chunk back. On a Friday-to-Friday view: Rubin Composite +0.59% on the week, but the dispersion underneath is wide. Interconnects +13.26%, Substrate +0.70%, Lithography +6.85% (Thursday close — Litho holds a few European names that don’t print Fridays). Memory −1.64% on the week, still +247% year-to-date. Wafer −9.36%. Packaging −4.13%. The leaders held; the broader complex rolled. That’s exactly what a stretched-tape consolidation looks like — not a clean roll-over, just enough red in the second tier to make the rally narrower week-on-week. Software is the brighter story underneath. The dispersion there is rewarding the names that own the AI workload versus the legacy SaaS being disrupted. But the headline still runs on the semis, and the semis are stretched.

The macro side is worse. Inflation prints came in hotter than expected. The ten-year Treasury is sitting at the 4.5% line. The thirty-year is camped above 5.1%. Both are at thresholds that historically punish duration assets — and equities, despite the way they trade in any given week, are duration assets. TLT, the long-bond ETF, is the cleanest single chart to watch right now: it closed the week down −2.81%, with a −1.48% Friday alone. That’s the bond market voting with its feet on the inflation print, and equities re-pricing off that base.

The breadth tell is the cleanest read of how stretched the leaders are. SPY closed the week +0.21% against RSP −1.24% — 145 basis points of gap inside five sessions, with the equal-weight version of the same index outright negative. Korea EWY −5.96% on the week (−6.12% Friday alone), Indonesia EIDO −5.04%, the rest-of-world VEU −2.74%, gold −3.80%. That kind of breadth divergence doesn’t last forever in either direction. It either widens into a parabolic top in a handful of names while the rest drift further, or it resolves with a catch-down in the leaders.

What gives the macro picture its quiet positive read is what the defensive sectors are doing under the surface. Healthcare and staples are showing relative strength this week — not in absolute terms, but in their leadership patterns. That tells you something important: the market is positioning as if these inflation readings are transitional rather than the start of a regime change. If high CPI were being read as persistent, the rotation into healthcare and staples would look like a panic move, and these sectors would be running with the heat. They’re not. They’re acting like a place to park while the binary plays out, not a place to hide in a crash. That distinction matters.

So we’re in the in-between. Stocks aren’t priced for rates to stay this high for long. If the bond market keeps pushing yields up — TLT lower — equities have to mark down. If the bond market relents and TLT bases, the relief is sharp. The market isn’t picking a side. Breadth is narrow because the marginal buyer can’t commit until the rate question resolves.

Next week is consequential because NVIDIA reports. NVDA earnings into a stretched semi tape with the ten-year and thirty-year at critical levels is the binary that defines the next four to six weeks. A clean beat-and-raise resolves the breadth question to the upside in the very short term — semis pull the index higher and the bond market gets ignored for another two weeks. A miss or a soft outlook flips the entire complex, and the breadth divergence resolves the other way.

Our expectation is more boring than either extreme: consolidation continues, the trend doesn’t break, the book holds its current posture into the print. The trim work was done last week. The roll work was done this week. The book is positioned for either tape — stretched-but-still-running, or beat-and-resolve. We’re not trading the print itself. We’re trading the second move after the print, when the dust settles and the leaders re-establish whatever they’re going to do for June.

Big picture: no heroes here. Trim what’s run. Roll up what you want to keep. Buy the materials and commodities exposure that’s been quietly leading. Sell premium on names you want to own cheaper. Read the bond market as the senior signal — anything below 4.5% on the ten-year is the relief-rally trigger; anything above 4.6% accelerates the duration repricing. Keep the cash dry for the post-NVDA reset.

The 3-engine architecture handles this without theatrics, the same way it handled last week. Volatility Harvesting opens NET and closes RKLB. Structural Narrative trims nothing and adds GLW where the chart finally gave us an entry. Tactical Growth rolls the option overlay up and out, then rotates the ETF basket into materials. Three engines, one rulebook, one tape.

Tags: AI Build-Out · Hypergrowth · Derivatives · Global ETFs · Global Tech 50 · Macro · Rates · Breadth · NVIDIA Earnings