By Thomas, Managing Director — Closelook Venture GmbH

February 16, 2026

The stock market is simultaneously pricing AI as the greatest wealth creator in history — and fleeing from it as the greatest destroyer of business models ever seen.

That’s not a contradiction. It’s a barbell. Capital is aggressively crowding into two opposite extremes — maximizing pure AI upside on one end, and seeking absolute physical safety on the other — while actively abandoning everything in between.

If you don’t understand which side you’re on, you’re probably in the middle. That’s the worst place to be right now.

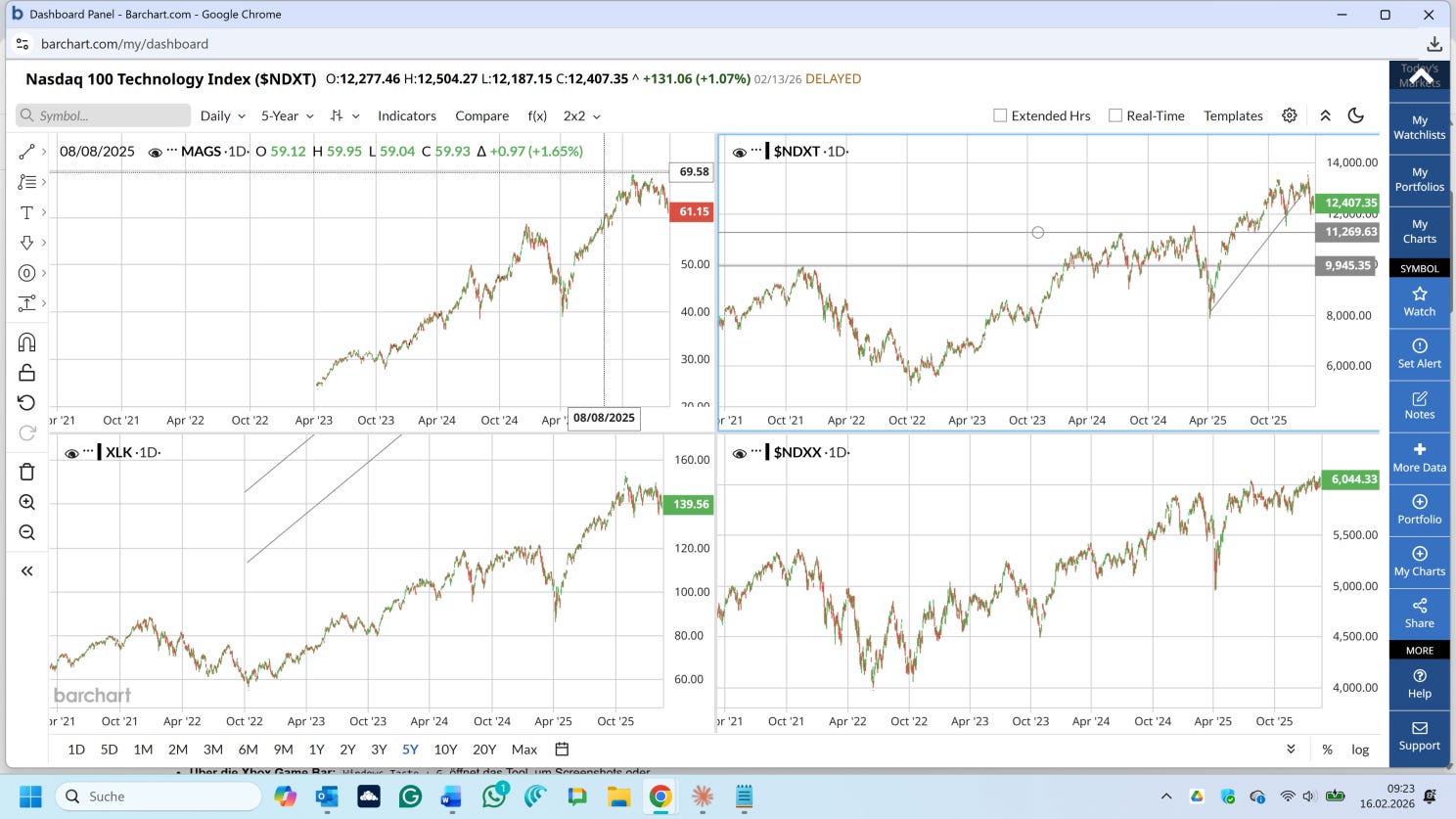

THE CHARTS TELL THE STORY

Look at these four charts. Read them in sequence, because the sequence is the narrative.

First, the Magnificent Seven story fractured. The concentrated mega-cap trade that carried markets for three years began to falter as investors questioned whether hyperscaler capex would translate into proportional revenue growth — or whether open-source models and efficiency breakthroughs (think DeepSeek) would compress the returns on that spending.

Then the Nasdaq 100 Technology Index ($NDXT) rolled over from its highs above 13,000, entering a volatile distributional pattern. The traditional growth engine of the market started coughing.

But here’s where it gets interesting. The Nasdaq 100 Ex-Tech Sector Index ($NDXX) — the non-technology components of the same Nasdaq 100 — broke out to all-time highs above 6,000. Decisively clearing resistance that had capped it for over a year.

This isn’t rotation out of growth. This is a rotation into durable growth. The market is repricing everything through a single filter: can an AI agent replace your business, or will AI make your business more profitable?

The answer to that question determines which side of the barbell you’re on.

WHAT CHANGED: THE AGENTIC TIMELINE PULLED FORWARD

Six months ago, the market consensus had agentic AI — autonomous systems that execute complex, multi-step workflows without human oversight — penciled in as a 2027 story. That was the comfortable timeline.

The logic was clean: Nvidia’s next-generation Vera Rubin architecture ships, data center infrastructure scales to accommodate it, enterprises begin cautious pilot programs, and widespread agent deployment follows 12-18 months later. Under that timeline, SaaS companies and IT consulting firms had breathing room. They could pivot, integrate AI features, and defend their moats.

Then the timeline broke.

Claude’s expanded agent capabilities, OpenAI’s autonomous tools, and a wave of agentic frameworks arrived 12-18 months ahead of schedule. Suddenly, enterprises weren’t talking about “AI strategy workshops” for 2027. They were deploying autonomous agents now — agents that could handle customer service tickets, write code, manage procurement workflows, and execute multi-step research tasks that previously required teams of people or expensive software subscriptions.

The narrative didn’t shift gradually. It snapped. The question went from “will AI justify the capex?” to “AI is disrupting faster and more broadly than anyone modeled.”

That single acceleration is the catalyst behind the barbell we’re living in.

SIDE ONE: THE AI INFRASTRUCTURE BUILD-OUT

On the aggressive growth side of the barbell, investors are riding the most capital-intensive technology deployment cycle in history.

The focal point remains the Rubin development timeline. NVIDIA confirmed at CES 2026 that the Vera Rubin AI architecture has entered full production — ahead of schedule. The market is aggressively investing along the entire chain of what it takes to power, house, and utilize these chips.

1st Derivative — Silicon and Foundries: The pure-play chipmakers and foundries at the top of the chain. NVIDIA, TSMC, and the companies that design and manufacture the actual compute.

2nd Derivative — Physical Infrastructure: The components required to make these chips operational. High-bandwidth memory (HBM4), silicon photonics for data center interconnects, liquid cooling systems for power-dense GPU clusters, and the server manufacturers assembling it all.

3rd Derivative — Real Assets: Data center real estate, nuclear power generation (Constellation Energy operates the largest US nuclear fleet and is a direct beneficiary), utility companies expanding grid capacity, and the raw materials — copper, aluminum, industrial gases — that physically build these facilities.

The New Layer — Agentic Infrastructure: The narrative has officially shifted from generative AI (chatbots and content creation) to agentic AI (autonomous systems executing complex workflows). The companies building semantic telemetry, secure API access layers, and enterprise data infrastructure to allow these agents to operate reliably are capturing the next wave of growth capital. This is where early-stage venture and growth equity are concentrating.

The market well understands this side of the barbell. What’s less understood — and where I think the bigger insight lives — is the other side.

SIDE TWO: HALO GROWTH — THE REAL STORY IN THE NON-TECH NASDAQ 100

Josh Brown of Ritholtz Wealth Management recently coined a term that’s gaining rapid traction: HALO — Heavy Assets, Low Obsolescence. Companies with massive physical footprints that AI cannot replicate or disrupt: energy, materials, food, logistics, heavy industry. An AI can’t pour concrete, fly a freight plane, or pump oil.

The HALO concept is correct. But most investors are stopping at the surface: “buy physical assets to hide from disruption.” That’s a defensive thesis. It misses the bigger opportunity.

The real story is HALO as a growth play.

Here’s the logic: the same agentic acceleration that is destroying the middle of the market is making these physical-world companies more valuable. They can deploy AI internally to expand margins — optimizing supply chains, reducing back-office headcount, automating logistics decisions, and improving demand forecasting — without any existential risk to their core product. An AI agent improves Walmart’s operations. It doesn’t make Walmart’s warehouses, trucks, and 4,700 stores obsolete.

These companies get the productivity upside of AI without the existential downside. That’s not defense. That’s a structural re-rating.

The NDXX Filter: A Growth Index for the Physical World

Here’s the practical filter I use: the Nasdaq 100 Ex-Tech Sector Index ($NDXX).

Why this index? Inclusion in the Nasdaq 100 already pre-selects for growth quality, liquidity, and market cap scale. These aren’t small-cap value traps or stagnant dividend aristocrats. They’re large-cap growth compounders that have earned their place alongside the world’s biggest technology companies.

Strip out the tech names using the ICB classification, and what remains is a curated universe of approximately 40 physical-world businesses. Apply a momentum filter within this universe — focusing on stocks with the strongest relative performance and positive trend — and the investable names cluster into clear buckets.

Not every NDXX constituent qualifies. Booking Holdings, Airbnb, DoorDash, PayPal, Workday, Cognizant — these are digital and services businesses that sit squarely in the “abandoned middle” despite being classified as non-tech. The NDXX is the starting universe, not the buy list.

Bucket 1: Consumer Staples with Tech-Platform Economics

Walmart ($WMT) — NDX weight 3.22%—the poster child. Ad revenue growing 53% YoY with 70%+ margins. AI agent “Sparky” handles 81% of product discovery. Just joined the Nasdaq 100 in January 2026, replacing AstraZeneca.

Costco ($COST) — NDX weight 1.36%. Membership flywheel, physical warehouse moat, consistent compounder.

PepsiCo ($PEP) — NDX weight 0.68%. Global distribution network AI can’t replicate, pricing power through cycles.

Monster Beverage ($MNST) — NDX weight 0.24%. Shelf space and distribution moat, approximately 13% earnings growth expected.

Mondelez ($MDLZ) — NDX weight 0.24%. Global snack brands, manufacturing, and distribution infrastructure.

Walmart is the poster child of the entire HALO growth thesis. It moved its listing from the NYSE to Nasdaq and joined the Nasdaq 100 in January 2026. That index swap alone tells you how the market classifies this company now.

Walmart is no longer a discount retailer. It’s a technology platform that happens to sell groceries. Walmart Connect, its advertising business, is growing 53% year over year and posting gross margins above 70%. Its AI shopping agent handles most product discovery. Its logistics network delivers to 95% of US households in under three hours. It’s using automation and AI to drive a 33% increase in net income while traditional competitors struggle with single-digit growth.

The other names in this bucket share the same structural advantage: physical distribution moats that AI can’t replicate, combined with massive internal operations that AI can optimize. Monster doesn’t need to worry about an AI agent disrupting energy drink consumption. But it can use AI to optimize its distribution routes, shelf placement, and demand forecasting.

Bucket 2: Healthcare — Defensive Demand Plus AI Productivity

Amgen ($AMGN) — NDX weight 0.60%. Biologics manufacturing moat, deep pipeline.

Gilead Sciences ($GILD) — NDX weight 0.58%. HIV/oncology franchise, recurring revenue base.

Intuitive Surgical ($ISRG) — NDX weight 0.52%. Robotic surgery installed base plus recurring instrument revenue.

Vertex Pharma ($VRTX) — NDX weight 0.38%. Near-monopoly in cystic fibrosis, expanding into pain.

Regeneron ($REGN) — NDX weight 0.26%. The Eylea and Dupixent franchises have strong pipelines.

GE HealthCare ($GEHC) — NDX weight 0.11%. Imaging hardware installed base plus AI diagnostics software.

IDEXX Labs ($IDXX) — NDX weight 0.15%. Veterinary diagnostics instruments plus consumables.

Healthcare delivered standout relative momentum over the past quarter, outperforming nearly every other sector. This isn’t just defensive rotation — three-month relative momentum is one of the more reliable forward-looking indicators, and in this case, it appears supported by fundamentals: defensive demand, improving earnings visibility, regulatory clarity, and the ability to deploy AI for productivity gains without the core service being at risk.

Intuitive Surgical ($ISRG) deserves special attention as a bridge stock — a company that sits at the intersection of both sides of the barbell. Its da Vinci robotic surgical systems are physical hardware with a massive installed base, generating recurring revenue from instruments and accessories every time a surgery is performed. But the robots themselves are AI infrastructure — they’re the physical platform through which surgical AI operates. Like Rockwell Automation in the industrial space, ISRG is both a HALO and an AI play.

GE HealthCare ($GEHC) follows a similar logic: a massive installed base of imaging hardware (CT scanners, MRI machines, ultrasound) with an emerging AI diagnostics software layer built on top. The hardware moat protects the business; the AI software layer is the growth catalyst.

Bucket 3: Industrials, Energy, and Power Infrastructure

Linde ($LIN) — NDX weight 0.68%. World’s largest industrial gas company. Essential to semiconductor fabs.

Honeywell ($HON) — NDX weight 0.46%. Industrial automation, building controls, aerospace.

Constellation Energy ($CEG) — NDX weight 0.31%. Largest US nuclear fleet. Direct data center power play.

Paccar ($PCAR) — NDX weight 0.20%. Premium truck manufacturing (Kenworth, Peterbilt).

Baker Hughes ($BKR) — NDX weight 0.18%. Oilfield services and energy technology.

Diamondback Energy ($FANG) — NDX weight 0.15%. Permian Basin pure-play.

Old Dominion Freight ($ODFL) — NDX weight 0.12%. Best-in-class LTL trucking network.

Fastenal ($FAST) — NDX weight 0.16%. Industrial distribution and on-site inventory management.

CSX Corp ($CSX) — NDX weight 0.23%. Rail network — irreplaceable physical infrastructure.

Ferrovial ($FER) — NDX weight 0.16%: toll roads, airports — pure physical infrastructure.

This is where the AI infrastructure story and the HALO growth story physically connect.

Linde ($LIN) supplies the industrial gases essential to semiconductor manufacturing. Every chip that powers an AI data center requires Linde’s products to be manufactured. Constellation Energy ($CEG) operates the nuclear plants that power those same data centers — Amazon signed an MOU with Dominion Energy to explore small modular reactor development in Virginia, and the entire hyperscaler complex is scrambling for reliable baseload power. Josh Brown explicitly cited Baker Hughes ($BKR) as a quintessential HALO stock.

The transportation and logistics names — Paccar, Old Dominion, CSX, Ferrovial — own physical networks that are effectively irreplaceable. AI can optimize routing and scheduling, but it cannot build a second Class I railroad network or replicate a national LTL trucking operation with decades of terminal infrastructure.

THE BRIDGE STOCKS: WHERE HALO MEETS AI

A handful of companies deserve a separate category because they sit directly at the intersection of both sides of the barbell. They own heavy physical assets (HALO), and they are active participants in the AI infrastructure build-out.

Rockwell Automation ($ROK) — Not in the Nasdaq 100, but the archetype of this bridge category. Just reported Q1 2026 with 10% organic sales growth, raised full-year EPS guidance, and Morgan Stanley lifted the price target to $460. Stephanie Link called it a “sleeper name for 2026” on CNBC. Rockwell is a physical industrial company whose products — factory automation, digital twins, AI-enabled process control — are the AI being deployed on production floors globally.

Intuitive Surgical ($ISRG) — Physical hardware that is simultaneously the platform for surgical AI.

GE HealthCare ($GEHC) — Imaging hardware plus AI diagnostics.

Constellation Energy ($CEG) — Nuclear power that directly enables the AI data center build-out.

These bridge stocks represent the most elegant expression of the barbell thesis: you don’t have to choose a side. You own the physical world and the AI future in a single position.

THE ABANDONED MIDDLE: WHERE CAPITAL GOES TO DIE

And then there’s the middle of the barbell. The hollow core. The valley of uncertainty where capital is being systematically withdrawn.

This abandoned middle consists of two groups:

The Actively Disrupted: Traditional Software-as-a-Service companies, legacy IT consulting firms, business process outsourcing (BPO) firms, and basic digital media. If an enterprise can deploy an autonomous AI agent to do the job of a $100/month software subscription or a human consultant, the moat collapses overnight. The agent doesn’t need a seat license. It doesn’t take lunch breaks. It doesn’t require a 12-month contract.

This is the SaaSpocalypse accelerated. What was supposed to be a gradual repricing over 2026-2027 is now happening compressed into weeks.

The “We Don’t Know” Group: Companies where it is entirely unclear whether AI will be a tailwind (boosting their productivity and competitive position) or a headwind (allowing competitors to steal market share cheaply). Investors cannot model the outcome, so they do the rational thing under uncertainty — they sell.

The result is valuation compression across the entire middle, regardless of individual company quality. Good companies are being punished alongside bad ones, because the market doesn’t have the patience or the analytical tools to distinguish between them.

THE WARNING: BENEATH THE SURFACE, THIS MARKET IS FRACTURING

Here’s where I want to leave you, because this is the part nobody is talking about.

The breadth data underneath this market is unlike anything we’ve seen since the dotcom bubble burst.

Right now, the materials sector has the highest percentage of stocks above their 200-day moving average, followed by energy and utilities. These aren’t the sectors that lead sustainable bull markets. They’re the sectors you find at the top when everything else has already broken down underneath.

Meanwhile, communications and technology — the sectors that have led every sustained advance for the past decade — are the only two where less than half of stocks sit above their 200-day averages. The engines of the bull market are running on fumes.

And here’s the statistic that should make you sit up straight:

Over the last 8 trading sessions, 115 stocks in the S&P 500 have declined 7% or more in a single day.

The historical average drawdown when that kind of internal damage occurs is 34%.

Right now, the S&P 500 is sitting just 1.5% below its all-time high.

Read that again. The surface is calm. The internals are fracturing. HALO stocks and a handful of mega-cap names are masking a rolling correction that has already begun beneath the surface.

THE SCENARIO NOBODY IS MODELING

The barbell works — until both ends need to reprice simultaneously.

Consider the sequence: AI infrastructure stocks have had an extraordinary run. They are due for a consolidation, a breather, a healthy pullback — call it what you will. This is normal and expected after any sustained advance.

When that consolidation comes, what catches the index? The disrupted middle cannot recover — those businesses face structural, not cyclical, headwinds. The HALO growth stocks provide a floor, but they don’t have the market cap weight to offset a meaningful correction in the mega-cap tech names that still dominate the Nasdaq 100 and S&P 500 by weight.

The result could be a violent index-level drawdown that feels disproportionate to the underlying economic reality. Not because the economy is broken, but because the market structure is fragile — propped up by a narrow set of winners on both ends of the barbell, with a hollowed-out middle that offers no cushion.

This is the most structurally fragile market since 2000. The parallels aren’t perfect — the AI build-out has real revenue and real earnings behind it, unlike the dotcom era’s vaporware. But the concentration of returns, the bifurcation of outcomes, and the internal damage beneath a calm surface are eerily similar.

POSITIONING

The AI revolution is real. The build-out is happening. The HALO growth thesis is sound. But revolutions create casualties, and this market is pricing in the winners while the losers quietly bleed out beneath the surface.

Here’s the uncomfortable reality: we are sitting just a few % below the all-time highs on the S&P 500, a bit more on the Nasdaq. The indices look fine. But at the individual stock level, hundreds of names are down 25-50% from their highs. For those companies and the investors holding them, this already is a bear market. The index is masking a level of destruction beneath it that we haven’t seen outside major drawdowns.

That creates a binary choice for investors:

If you can pick stocks, be on the right side of the barbell. Own the AI infrastructure, building the future. Own the physical-world HALO growth companies that AI makes more profitable. Use the NDXX as your screening universe, apply a momentum filter, and stay far away from the abandoned middle — the SaaS, consulting, and digital services names facing structural disruption, not cyclical weakness. Some will pivot successfully, but identifying which ones in real time is a coin flip, and the market is not rewarding uncertainty.

If you’re not sure, you can pick the right stocks — own the index. The major indices are holding up precisely because they are market-cap weighted toward the winners on both sides of the barbell. The S&P 500 and Nasdaq 100 are, by construction, self-cleansing — they rotate toward the names that are working and away from the names that are not. In a market this bifurcated, the index may be the safest way to stay invested without picking the wrong side.

What you cannot afford to do is hold a portfolio of individual stocks in the middle and assume you’re “diversified.” Diversification across the abandoned middle is not safety — it’s concentrated exposure to the one part of the market that is structurally impaired.

This is true for so-called value stocks as much as for former growth compounders. The index is a mask. But sometimes, the mask is the trade.

Thomas is Managing Director at Closelook Venture GmbH, publishing structural market intelligence, AI supply chain analysis, and trading signals at closelook.io and on Substack.

This analysis is for informational purposes only and does not constitute investment advice. Past performance is not indicative of future results.

Closelook Venture GmbH (CLV) and the author believe all information contained in this article to be accurate, but cannot guarantee its accuracy. None of the information in this article or any opinions expressed constitutes a solicitation of the purchase or sale of any securities or commodities.

This is not personalized advice. Investors should conduct their own research and/or consult an investment professional when making portfolio decisions. Past performance of any investment is not a guarantee of future results. CLV representatives or clients may have positions in securities discussed or mentioned in its published content.