SK Hynix’s American depositary receipts start trading on Nasdaq today under SKHY — $26.5 billion, the largest US listing by a foreign company on record, priced at $149 apiece: a 2.9% premium to Seoul’s close, where deals of this size normally price at a discount. That alone would make it a session to watch. But the debut is also the right moment to take the memory trade apart, because the three companies that dominate it are not interchangeable ways of owning the same thesis.

Memory used to be treated as a commodity business. Buy the producers when DRAM prices collapsed, sell them when new capacity arrived, and never confuse a temporary shortage with a durable competitive advantage. AI is changing that framework. The critical product is no longer simply another unit of DRAM: high-bandwidth memory sits beside the accelerator, determines how quickly data reaches the processor and increasingly constrains the performance of the entire AI system. That turns memory from a replaceable component into part of the computing architecture.

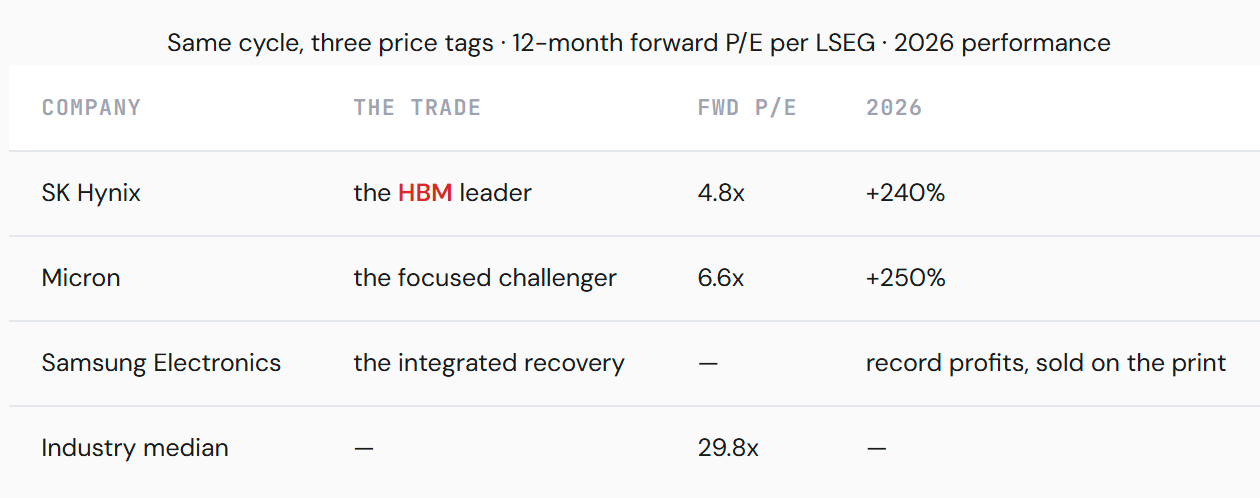

And yet the market prices the three companies as if they lived in different industries.

Both leaders are up roughly 240–250% this year — and the valuation gap between them has not budged. Analysts call the reason “access and familiarity”: the Korea discount, the tendency of Korean companies to trade below global peers on governance concerns and limited accessibility for US funds. Today’s listing is the first live test of whether that gap is structural or just friction.

SK Hynix: the leader, defending

SK Hynix is the cleanest expression of the HBM thesis. It built the strongest position through the HBM3 and HBM3E generations, carried that customer credibility into HBM4 — completed early, shown in 12- and 16-layer products, HBM4E samples shipped to major customers in June — and holds a multi-year technology partnership with NVIDIA covering next-generation memory and AI-driven manufacturing.

This matters because qualification is becoming a moat. HBM is not bought from a catalogue and inserted into a server at the last moment. Memory, packaging, thermals, power consumption and accelerator design have to be coordinated years in advance; a supplier already embedded in the customer roadmap is difficult to displace merely by offering additional capacity.

The listing itself is less about money than about who can buy. S&P expects the company’s capex of ₩50–70 trillion a year to be funded overwhelmingly from internal cash flow — the $26.5 billion is welcome, but the durable prize is direct access to the deepest capital pool in the world. What the leader is defending: a market share of roughly 57% last year, heading toward ~50% this year and the low-40s over time as competitors scale. The real debate, as one analyst put it, is less about share and more about who can bring on the capacity to meet demand at all — even announced fab expansions look insufficient through the end of the decade.

SK Hynix is not the turnaround story. It offers the strongest established HBM position, the deepest exposure to NVIDIA’s accelerator cycle, the clearest link between HBM pricing and profitability — and the greatest risk that leadership is already reflected in expectations. At 4.8 times forward earnings, the market appears to disagree with that last point. That is the anomaly the debut gets to resolve.

Micron: the challenger, at a trillion

Micron is sometimes described as the smaller third player. That description misses what has changed — including on the tape: Micron closed yesterday at a $1.12 trillion market capitalization, up +4.5% on the day and roughly ten times its 52-week low, and still trades near 6.6 times forward earnings.

The company has begun volume shipments of its 36GB 12-layer HBM4 for NVIDIA’s Vera Rubin platform, with base logic die and DRAM core dies designed and manufactured internally. Its latest quarter showed record revenue, gross margin and earnings; data-centre revenue passed a $100 billion annualized run rate and data-centre SSD revenue more than doubled sequentially.

Micron’s distinction is not that it possesses SK Hynix’s scale in HBM. It is that it combines credible leading-edge technology with a relatively focused corporate structure. Unlike Samsung, it is not diluted by smartphones, displays, appliances and a foundry operation; unlike SK Hynix, it still has room to take meaningful incremental share from a smaller base — plus full participation beyond HBM through server DRAM, low-power memory and enterprise SSDs, and the most direct exposure to US data-centre investment. Micron is not a weaker version of SK Hynix. It is the focused challenger, with operating leverage if technology, qualification and capacity let it close the gap.

Samsung: the integrated recovery

Samsung is the hardest of the three to classify — the largest and most diversified group, spanning conventional memory, HBM, logic, foundry, advanced packaging, phones, displays and consumer electronics. The diversification obscures the memory thesis: a strong HBM quarter does not flow through consolidated results the way it does at SK Hynix or Micron.

But look at what just happened. Samsung’s second-quarter flash showed ₩89.4 trillion in operating profit — about $59 billion, a nineteen-fold increase on the year, past NVIDIA to make it the most profitable company in the world for the quarter. Its chip division has said 2026 alone should out-earn the division’s entire 40-year history combined. And the stock fell 7% on the print.

That reaction is the Samsung trade in one line: the market pays for execution it can verify, and Samsung’s gap between theoretical capability and demonstrated execution is still the widest of the three. The company began mass production of HBM4 in early 2026, expects HBM sales to more than triple this year, and has shipped 12-layer HBM4E samples — positioned for the same Vera Rubin platform. It also possesses something neither competitor can replicate: memory, logic manufacturing, foundry services and advanced packaging inside one organisation. Vertical integration becomes a moat only when process, base die, packaging, thermals, yields and qualifications work together; until then it is organisational complexity. The old framing — SK Hynix leads, Micron follows, Samsung has failed — is becoming too simple. Samsung is the recovery and optionality trade: the company that could change the competitive structure most dramatically if its assets finally operate as one system.

The three trades

Reduced to one line each: SK Hynix — pay for leadership. Micron — pay for focused growth and potential share gains. Samsung — pay for recovery, integration and strategic optionality.

They also respond differently to the same news. Higher HBM prices and stronger NVIDIA volumes flow most directly into SK Hynix. Evidence of share gains, expanding US capacity and broader data-centre demand matters disproportionately for Micron. Successful qualification, improving yields or a large custom-accelerator contract could produce the largest change in perception at Samsung — as the −7% answer to a record quarter shows, perception is the variable with the most room to move.

The larger point

The memory market is not becoming less cyclical. Capacity still matters, customer concentration still matters, and every premium product eventually attracts investment and competition. But the cycle itself is changing: HBM consumes more wafer capacity than conventional DRAM, requires complex stacking and packaging, and must be co-designed with the processor and system around it. Supply cannot respond as quickly or as uniformly as it did in the old commodity-memory cycle.

The decisive question is no longer just who can manufacture the most bits. It is: who can deliver the right memory, at the right power and thermal envelope, qualified for the right accelerator, at the moment the next architecture enters production? Today SK Hynix has the strongest answer, Micron the clearest opportunity to gain, Samsung the widest range of assets for a comeback.

Three memory companies. Three different investment cases. Three very different ways to participate in the AI factory — and as of today, all three of them price in dollars on American exchanges. Whether that closes the gap between the price tags is this session’s open question.