Trump Rally Loses Steam: Signs of a Bear Market Lurking

Higher Rates and Technical Breakdowns Point to Potential Market Reversal

(1) What's the buzz?

The latest CPI report indicates that inflation might persist above the Fed's 2.0% target. In October, the headline and core CPI inflation rates increased by 2.6% and 3.3% year-over-year, respectively.

Although goods prices continue to decline, supercore inflation, rent inflation, and wage growth all saw an increase last month, suggesting they are becoming stuck at relatively high levels.

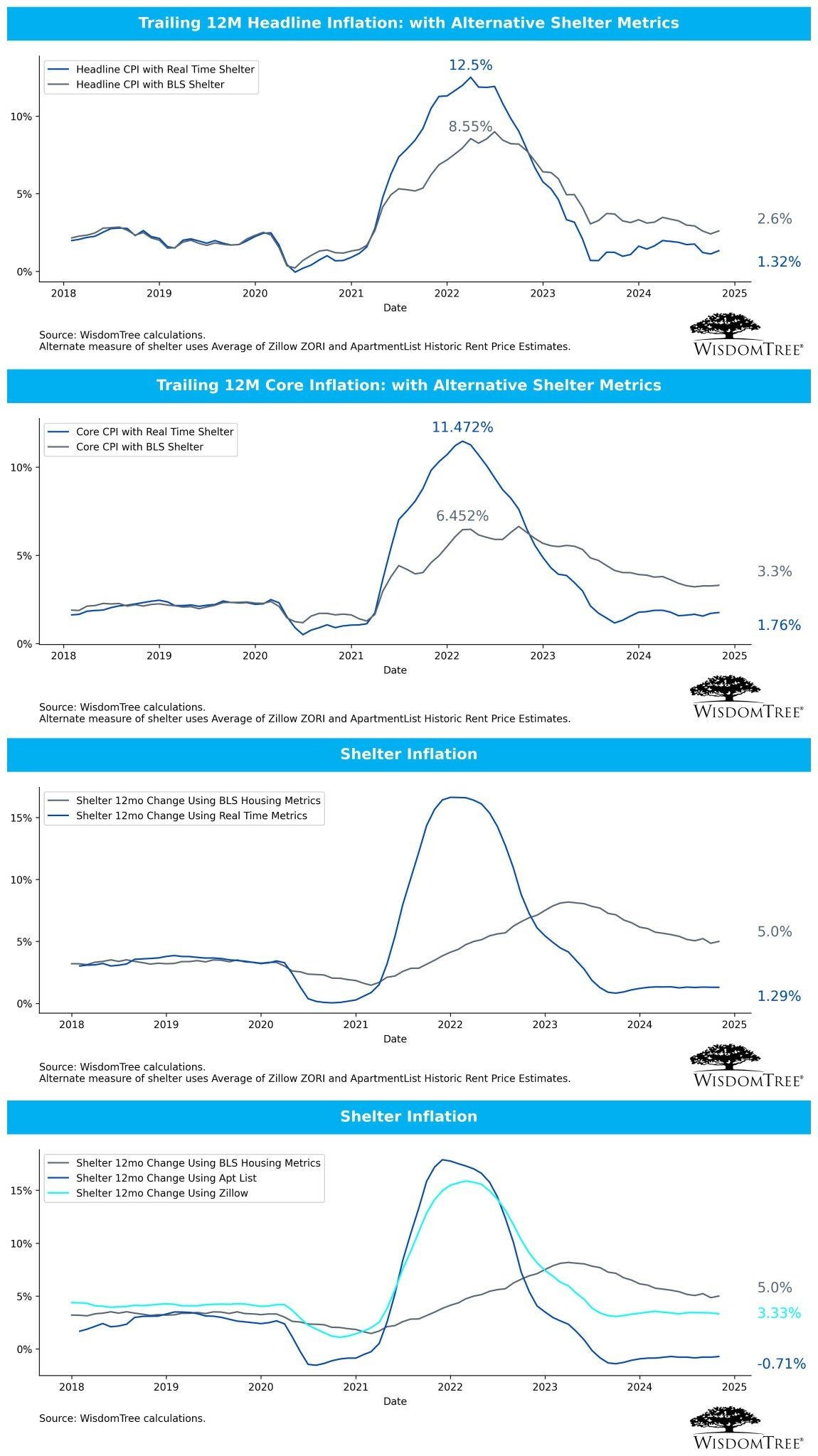

The charts above demonstrate a significant divergence between inflation measures using real-time shelter data versus the official BLS shelter metrics. When using real-time shelter data, inflation rates are notably lower:

Key Observations

Headline CPI

Real-time shelter metrics show headline inflation at approximately 1.32%, well below the 2% target, while BLS shelter metrics indicate 2.6%

Core CPI

Using real-time shelter data, core inflation is around 1.76%, compared to 3.3% with BLS shelter metrics.

Shelter Inflation

The most dramatic difference appears in shelter inflation itself, where real-time metrics show approximately 1.29%, while BLS housing metrics indicate about 5.0%

The real-time shelter metrics from Zillow and ApartmentList data suggest significantly lower inflation rates than the BLS methodology.

This divergence suggests that using more current shelter data would place overall inflation comfortably below the Fed's 2% target, in contrast to the higher readings produced by the BLS methodology.

(2) So what?

Sticky inflation is one reason why the Fed may not cut interest rates as much as anticipated by the market in 2025. More than fifty percent of the recent advance of the SP 500 is due to multiple expansion and not rising earnings.

Higher rates may lead to multiple contraction in 2025, offsetting the effects of growing earnings. No matter which valuations to apply, the US stock market is expensive.

(3) Now what?

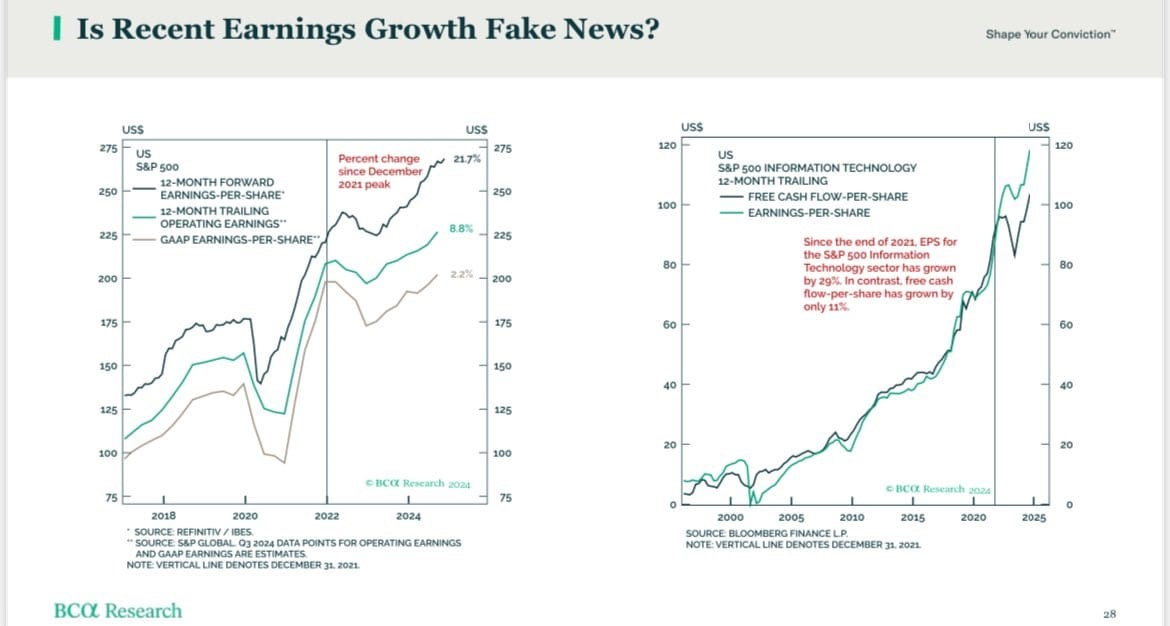

This is especially true when earnings growth is not as stellar as it seems when looking at GAAP earnings growth.

The image above shows two financial charts from BCA Research about S&P 500 earnings trends:

Left Chart Analysis

Shows three earnings metrics from 2018-2024:

12-month forward earnings-per-share

12-month trailing operating earnings

GAAP earnings-per-share

Indicates a 21.7% percent change in 12-months forward earnings per share change since December 2021 peak

Operating earnings only show an 8.8% increase

GAAP earnings only show a 2.2% growth

Right Chart Analysis

Focuses specifically on S&P 500 Information Technology sector

Compares two metrics from 2000-2025:

Free cash flow-per-share

Earnings-per-share

Notable divergence since the end of 2021:

EPS has grown by 25%

Free cash flow-per-share has only increased by 11%

Shows a significant upward trend in both metrics since 2000, with particularly steep growth after 2020

Key Observations

Recent earnings growth may be a bit fake news given the much lower GAAP earnings growth figures and the gap between EPS growth and free cash flow growth in the technology sector.

(4) And next

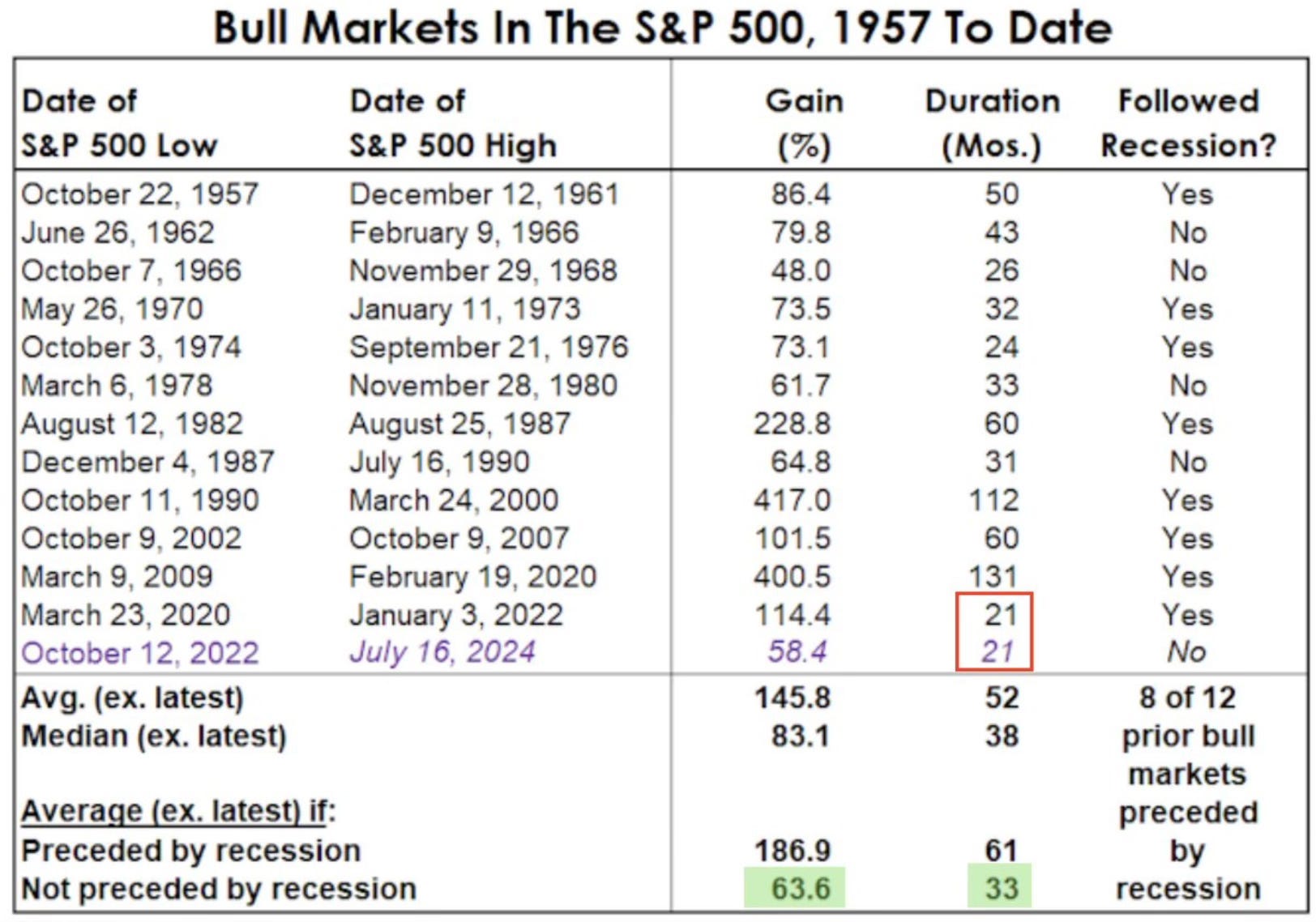

Seth Golden points out in the table below that the average length of a bull market that was not preceded by a recession is 33 months. That would take this bull market cycle out until May 2025 only.

Here is a close look at where this current bull market is compared to other bull markets dating back to 1957. The table is from the summer of 2024, so please add four months to the current bull market.

Right now, the length of this bull market (25 months) is four months longer than the shortest bull market in history, the last one, which ended in January 2022.