Why Another Leg Down in SaaS and Software May Be in the Making

The first leg down in SaaS and software was mainly about duration.

The market did not immediately decide that all software earnings were impaired. It decided that those earnings could no longer be discounted with as much confidence as before. AI introduced uncertainty around product durability, pricing power, competitive moats, seat-based models, and long-term customer retention.

As a result, investors shortened the valuation horizon they were willing to assign to future software cash flows.

Software stocks, while earnings held up. That was derating step one.

The next leg down, if it comes, would be different. It would not only be about a shorter duration over which to discount future earnings. It would be about the earnings base itself becoming less reliable at the same time that discount rates remain elevated.

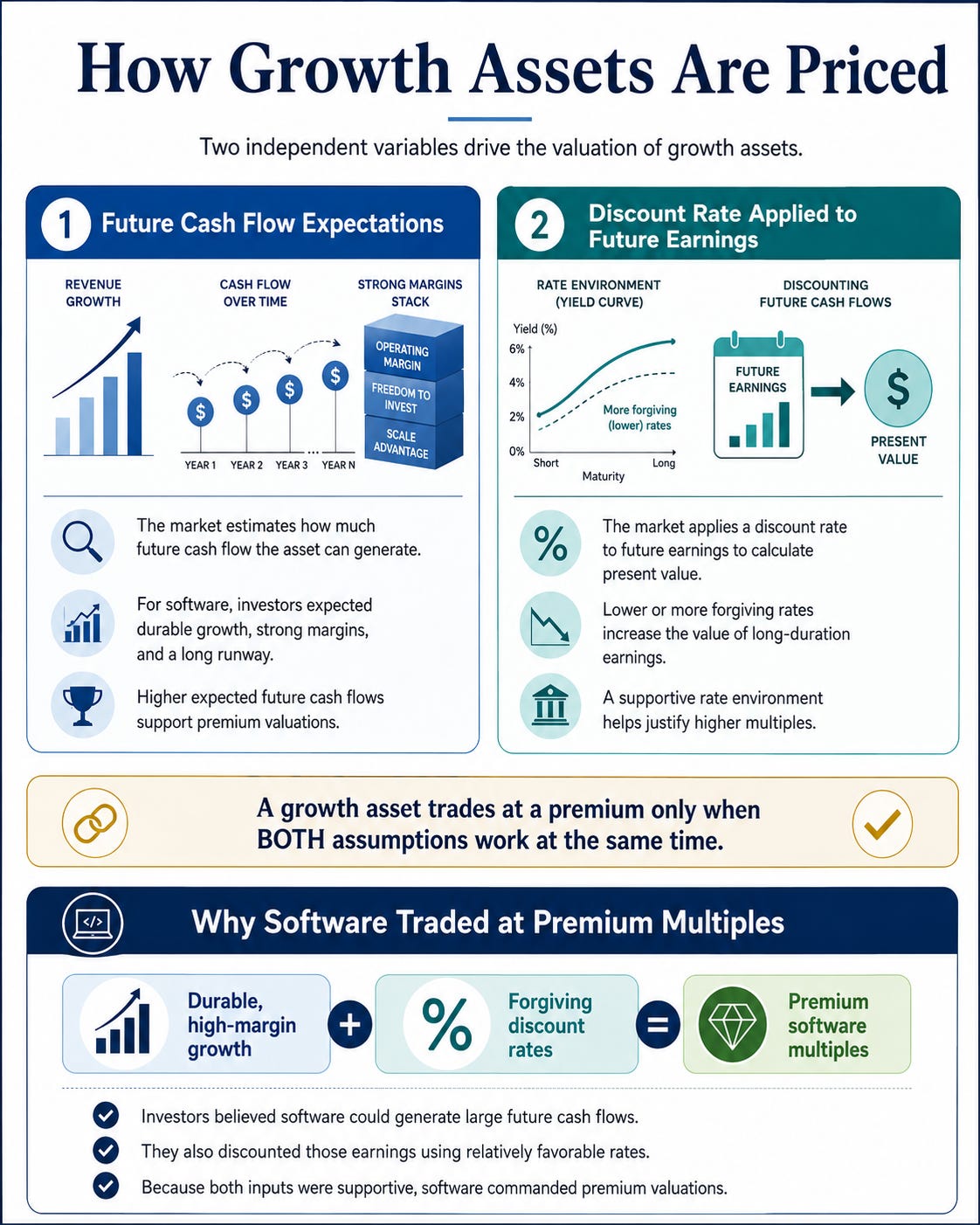

Growth assets price two independent variables simultaneously. The first is the future cash flow the asset is expected to generate. The second is the discount rate applied to that future cash flow. Software traded at premium multiples because both assumptions worked in its favor for a long time. Investors believed in durable, high-margin growth, and they applied relatively forgiving discount rates to those future earnings.

That combination is now under pressure.

The rates backdrop has changed again. Bank of America now expects three Federal Reserve rate hikes in 2026, while Deutsche Bank has reportedly moved in a similar hawkish direction, with two hikes expected this year. The exact number matters less than the direction of the revision. The market debate has shifted from “how many cuts?” to “could the Fed be forced to hike again?”

That matters for SaaS and software because these are long-duration equities. Their valuation depends heavily on future cash flows. When short and intermediate rates rise, the discount rate applied to those future cash flows rises as well. That lowers present value and compresses multiples.

The bond market is also sending a warning. The IEF and IEI charts point to pressure on intermediate-duration Treasuries, which implies higher yields in the belly of the curve. If the belly and the short end rise quickly while the long end stays closer to current levels, the yield curve flattens.

That is not a good scenario for SaaS stocks.

A flattening curve led by rising short and intermediate rates means investors are being asked to discount future software earnings at higher rates. At the same time, AI is making those future earnings harder to underwrite. The market would no longer be applying a higher discount rate to the same earnings stream. It would be applying a higher discount rate to a less certain earnings stream.

Investors may quickly think back to 2022. That year, long-duration growth assets were hit hard as rates rose and valuation multiples reset. The risk today is not an exact replay of 2022. The setup is different. In 2022, the pressure came mainly from the discount-rate side. Today, the discount-rate pressure may be returning while AI creates a second pressure point around earnings durability.

That is where the second leg becomes dangerous.

Higher rates attack the multiple. AI uncertainty attacks the earnings stream. Together, they create the possibility of a second derating phase.

In some software categories, AI is not just a productivity enhancer. It is a force that can change the economics of the product category itself. If AI lowers switching costs, automates workflows, compresses seat-based pricing, or makes legacy software functions easier to replicate, then the expected cash flow pool changes.

Operating companies inside a growth sector face their own incentive problem. Maintaining competitive position in an AI-driven environment requires sustained investment. Companies must spend on infrastructure, model integration, product redesign, security, distribution, and customer retention. For the largest platforms, this means massive capital expenditure. For smaller SaaS companies, it can mean higher R&D intensity, margin pressure, or a greater need to access external capital.

At the same time, commoditization can accelerate. When product performance converges across competitors, pricing power moves from seller to buyer. Customers become less willing to pay premium prices for software that looks increasingly substitutable. Margin compression follows. Compressed margins reduce the cash flows that originally justified high multiples.

The same investment required to defend a competitive position can therefore produce lower returns if the product category itself becomes more commoditized.

This risk is not limited to unprofitable SaaS. It can also affect profitable software companies if investors begin to question whether margins, growth rates, retention, and pricing power are sustainable. The market does not need earnings to collapse for multiples to compress. It only needs confidence in the durability of those earnings to fall.

The pressure may also extend to parts of the Magnificent Seven. The issue is not whether these companies are strong. They are. The issue is whether the market has already priced in future AI benefits in current valuations, even as the cost side becomes more visible. If AI capex rises faster than monetization, or if returns on that spending become harder to prove, then even dominant platforms can face multiple pressure.

This is why the rotation toward hardware, infrastructure, semiconductors, networking, data centers, power, and cooling has a structural logic. These businesses monetize the AI race itself, not necessarily its final winner. They serve all competing architectures and platforms. Their demand is easier to verify because it depends less on which application-layer company ultimately captures the profit pool.

That is the key distinction.

Software investors must underwrite who wins, how much pricing power remains, and how durable the earnings stream will be. Infrastructure investors can underwrite the arms race.

The conclusion is simple: the first leg down in SaaS and software was about duration risk. The next leg down may be about earnings risk, meeting rate risk.

When future cash flows become less certain, and the discount rate rises simultaneously, the adjustment is not additive. It is multiplicative.